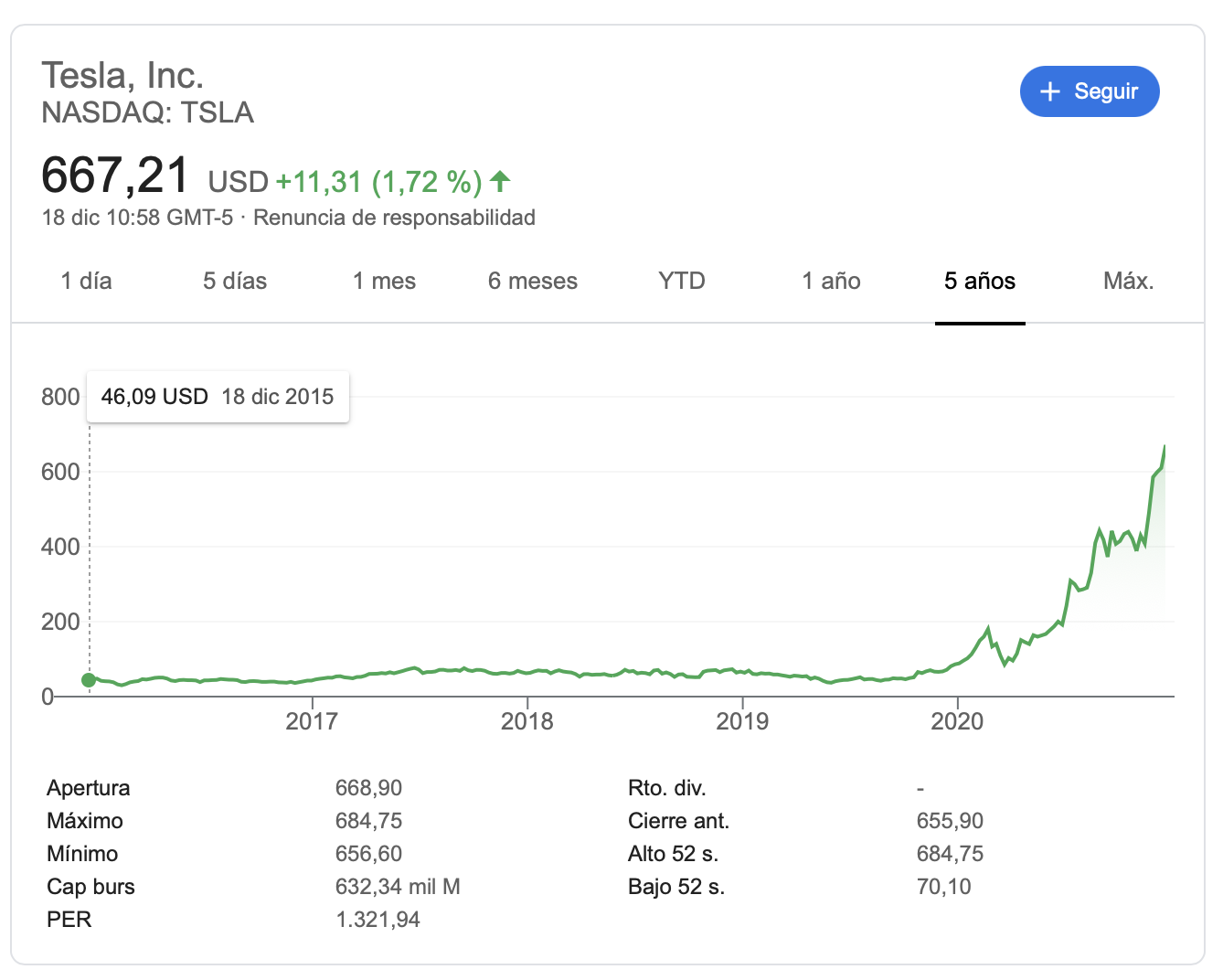

Al final he comprado el iShares, a lo Burry, y con margen, a la espera todavía de que Hacienda me devuelva el dinero de 2019 para liquidar mi saldo negativo en IB.

Bueno, el corto tenía un análisis sólido detrás, las hipotecas -producto de largo por excelencia- estaban pensadas (analizadas) a corto, con improbable riesgo de no caerse con como un castillo de naipes como ocurrió, si un tipo analiza algo, y ve y cree que no funcionará en el futuro lo lógico es invertir en ello, precisamente de eso se trata la inversión, de creer tu tesis y apostar en que se cumplirá, si tu tesis es contraria a tendencia o mercado has de ponerte enfrente, pero si analizas algo y luego no haces caso del análisis, para qué lo haces ¿qué sentido tienen entonces hacer análisis?

Burry puso mucha pasta porque la consiguió, entiendo que si hubiera tenido menos no habría conseguido un producto ad hoc, y si consiguió el dinero tuvo que convencer a gente cosa que al parecer no fue fácil y lo hizo con un análisis.

Completamente de acuerdo, nada es exacto y como es conocido tuvo que bregar con ello:

Cita de wikipedia (La negrita es mía): “ Burry sufrió una revuelta de inversores, donde algunos inversores de su fondo temían que sus predicciones fueran inexactas y exigieron que se les permitiera retirar su capital. ”

En mi opinión solo un genio hace eso y los genios no son personas ‘normales’ si así fuera no serían genios, serían normales

A mi también me parece un crack Michael Burry, visto desde fuera puede parecer una apuesta loca, pero el tipo entró al detalle del sistema financiero, empezando por estudiar algunas inmobiliarias y aseguradoras, hasta acabar entrando en el detalle de las hipotecas, los hipotecados, las agencias de calificación…

Dejo un extracto de una entrevista, negritas mías para quien no quiera leerlo entero. Abajo el enlace a la web de donde está extraído

The way I got involved in housing at all was by — I was a stock picker, pretty much a long-oriented stock picker. And I started looking at home builders which were all in the press. A lot of people were saying that these were undervalued securities. So I looked at them and I decided that I didn’t think they were terribly attractive because they were benefiting tremendously from the increase in land values on their inventory and this was contributing to a great extent to their returns. And it led me to — So I didn’t think too much of the home builders and I let them go, but I wasn’t really thinking that housing was gonna collapse.

In looking them, I started thinking about how housing is financed. This was 2002-ish. And I started looking at the mortgage insurers and PMI in particular. Then I compared it to MGIC, which is another mortgage insurer, and I just read their filings. I noted that they were getting involved in so-called insuring negotiated transactions or bulk transactions. So, at the time I didn’t even know what they were. So I said OK what are these? But I know insurance — I like to study insurance. So I did notice that their strength, from their typically line of business to go into the auction — basically insure through an auction process that doesn’t guarantee them any unusual knowledge that might advantage them in their underwriting.

So, I moved to looking at the mortgage pools and starting to understand how they work. This was ’03, by spring of ’03. What it did is, it lead me to start getting involved in the credit default swap markets. Well, partly, so that’s another story. But in understanding RMBS, it wasn’t information that I used too much other than to just monitor the market for a while. I actually instead moved to purchasing some credit default protection on certain financial companies and that was a result of something else. So that’s — 2003 is when I first started credit derivatives and I learned a lot about the credit derivatives market over the year or two leading up to 2005. That’s when we did all these ISDAs and that sort of thing.

I was particularly interested in the history of the housing or the history of the derivatives market and how it developed. And so that’s also another part… And after the tech crash, 9/11, WorldCom, the interest rates obviously fell and there was other mechanisms used, as well, to put credit into the system. And I noticed that it was affecting the housing markets through the types of mortages that were being introduced. So I termed that “extension of credit by instrument” because once rates had fallen to a certain level — mortgage rates were already at forty year lows, they weren’t going any lower — how do you stimulate demand? And one way is to create different mortgage products or affordability products to essentially allow home prices to rise.

So on the back of this easy credit, there’s also this whole issue of how mortgages are being originated, typically through a mortgage broker into an originate and sell model — mortage originator that would then sell off the mortgages to Wall Street, increasingly so. And I saw all kinds of problems with agency risk, moral hazard, and adverse selection throughout that whole process. And when you piled all these things up, what I came to have significant worries about the housing market in ’03. And what I turned to investors — it’s a basis for concern. I didn’t think that — warn that these were multi-decade cycles and that we shouldn’t jump to any conclusions.

2003 saw the introduction of interest only mortgages. I watched those with interest as they migrated down the credit spectrum and into the subprime market. And when they had migrated down the credit spectrum about as far as they could go, to the extent they could, other products were created. Notably, in my view, the option ARM or negatively amortizing mortgage, which I viewed as the most toxic mortgage that could ever be imagined. And, I thought at that point since home prices had been rising at a rapid rate, essentially on the back of easy credit, with virtually no accompanying rise in our wages or incomes, that I came to a judgment: in 2007, 2 years hence, there would be a final kind of judgment on housing when those people taking out those two year ARMs, go to seek refinance. So I was watching these mortgage pools, and it came to a point where I paired my understanding of the derivatives market to what I saw in the mortgage pools.

Artículo completo

Y mención especial a la película The big short (La gran apuesta en español, supongo que de haberla titulado El gran corto no lo hubiéramos entendido más que 4 frikis)

Cuando se reúne en Goldman Sachs y les dice “todo el mundo está equivocado” y negocia los CDS me parece fuera de serie. No hay que olvidar que Burry tiene síndrome de Asperger y eso dota a algunas personas el don de la concentración

Interesante @emgocor es una temática que hace un par de años leí que podría resultar interesante para invertir…

Una pregunta @emgocor y disculpa mi ignorancia…estás empresas del agua no están algunas o la mayoría en índices como Sp500 o Msci World, Vanguard Total Stock Index?

También lo que dices tiene sentido, el riesgo de ir contramercado o contra cualquier cosa que tenga mucha fuerza económica o social es un poco “temerario” pero como todo es porque se adelantan a su tiempo, de hecho Burry tuvo éxito por eso mismo por anticipar algo que iba a ocurrir, acertar con los tiempos era difícil y sufrió lo suyo por ello, pero cuando ya era evidente lo que iba a ocurrir los bancos le ofrecieron comprar la posición, ya era tarde para ello. Hay que tener la visión y la decisión.

Entonces quizás sea como sobreponderar un sector o temática ? como pudiera pasar con otros ahora de moda ( biotecnología, ciber seguridad, iCloud,…) apostando que en el medio/ largo plazo lo harán mejor que el índice en el que ya están incluidos…?

En un mundo apocalíptico el agua es más importante que el Oro…

El Oro solo conservaría lo justo para comprar bienes indispensables, como Víveres o un billete de avión para salir corriendo por si nombran al Chepas Presidente.