Por lo menos estos trabajan…

Demasiadas SBC:

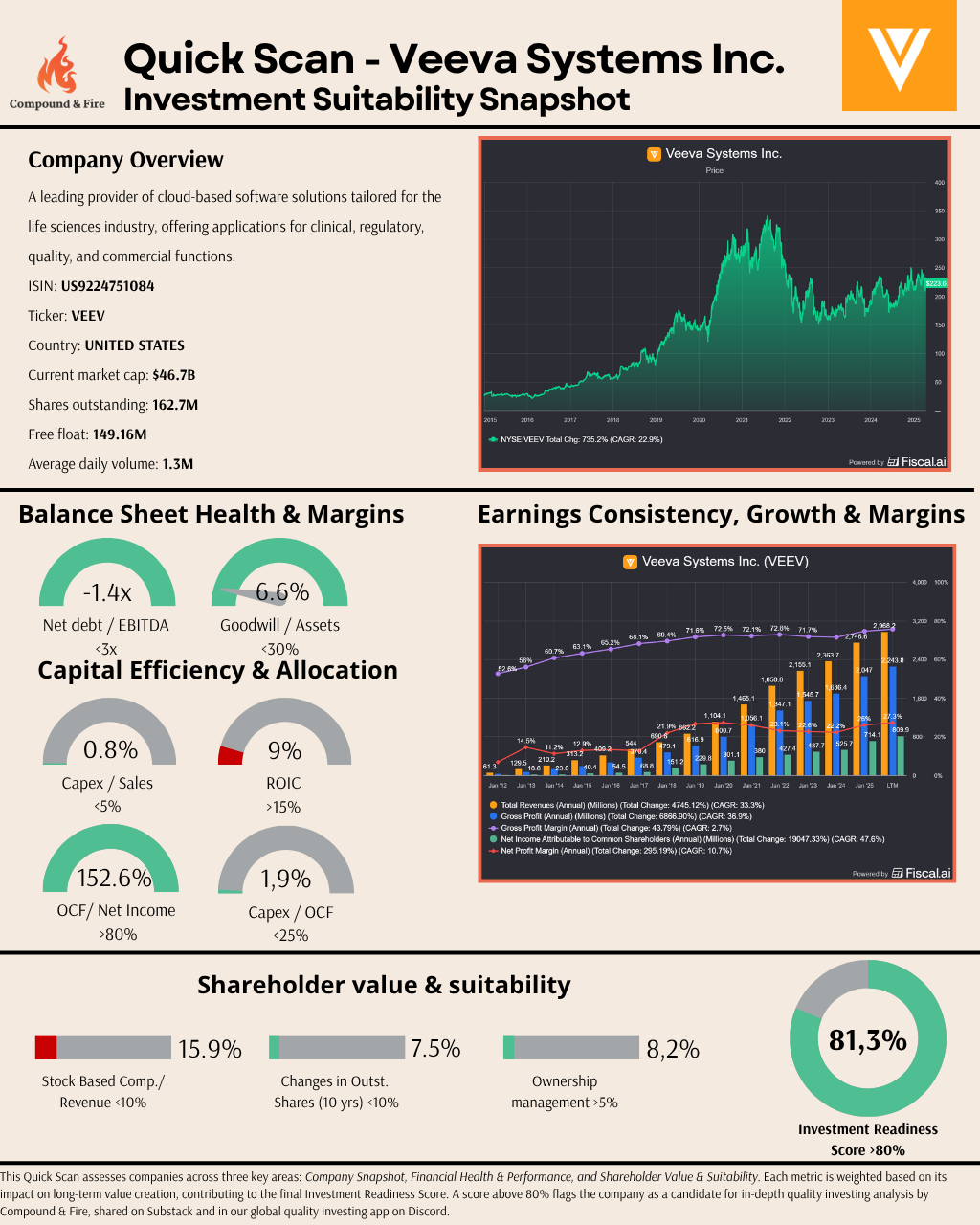

- Net Debt / EBITDA: -1.4x (100/100) – Pristine balance sheet with net cash position, providing exceptional financial flexibility.

- Intangibles / Assets: 6.6% (95.6/100) – Low ratio reflects asset-light SaaS model with minimal reliance on acquisitions.

- Capex / Sales: 0.8% (97.0/100) – Extremely capital light for a software business, with negligible reinvestment needs.

- Return on Invested Capital: 9.0% (48.1/100) – Looks like a low ROIC for a high-growth SaaS leader, but quite sure when making adjustment for acquisitions and / or R&D that the real ROIC will be higher. That’s a next step within the deep dive.

- OCF / Net Income: 152.6% (98.2/100) – Outstanding cash conversion, far exceeding earnings due to efficient operations.

- Gross Margin: 74.5% (91.5/100) – Elite margins typical of premium life sciences SaaS.

- Net Profit Margin: 26.0% (84.4/100) – Exceptional profitability driven by subscription recurring revenue and pricing power.

- Revenue 10YR CAGR: 21.3% (90.9/100) – Consistent high growth over a full decade, fueled by life sciences digital transformation.

- SBC / Revenue: 15.9% (21.9/100) – Elevated stock-based compensation reflects tech talent retention costs.

- Changes in Outstanding Shares: 7.5% (85.0/100) – Moderate share dilution over 10 years, aligned with growth incentives.

- Ownership Management: 8.2% (81.3/100) – Meaningful insider alignment, with founder-CEO Peter Gassner holding significant stake.